On Wednesday, the Los Angeles Times ran an investigative report on school districts‘ use of “capital appreciation bonds” to fund building construction and maintenance. Unlike standard school bonds, the capital appreciation bonds (“CABs”) have a prolonged and postponed repayment schedule that can drag out to as long as 40 years. They’re structured to skirt limits imposed by the state on how much school districts can borrow and how much tax they may levy.

CABs have been receiving increasing scrutiny across California ever since the Voice of San Diego website published an investigation into one such bond issued by Poway Unified School District’s in August. Poway Unified had borrowed $100 million, but because repayment was scheduled far into the future — with interest piling up in the meanwhile — it will end up paying nearly $1 billion to service that debt. The backlash from that story has riled up everyone from the Democratic establishment to the Howard Jarvis Taxpayers’ Association.

“The school boards and staffs that approved of these bonds should be voted out of office and fired,” California Treasurer Bill Lockyer told the LA Times.

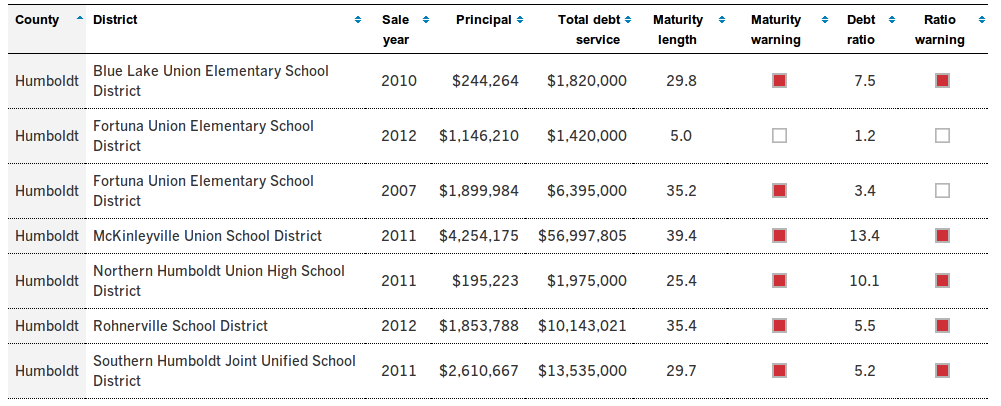

What of Humboldt County? The Times includes a searchable database of all school districts in California that have issued capital appreciation bonds. Six Humboldt County school districts make the list:

Of these six, Fortuna Union’s bonds are pretty blameless. The debt ratio of these bonds — the amount taxpayers will eventually pay as compared to the amount the district originally borrowed — is pretty much in keeping with more conventional bonds. Rohnerville and Southern Humboldt have moderately high debt ratios. But the other three — Blue Lake Union, Northern Humboldt Union and McKinleyville Union — are way off the charts.

The case of the McKinleyville Union School District is especially striking. In 2008, residents of the district just barely approved Measure C, which authorized the district’s board of trustees to offer up to $14 million in bonds. (The measure required a 55 percent yes vote to pass.) Of that, the board elected to offer $4.2 million in the form of capital appreciation bonds. Since that debt was structured over a 40-year period, with interest accruing all the while, taxpayers in the district will eventually be on the hook for over 13 times that amount — a stunning $57 million in total.

Richard Hanger, the Humboldt County Office of Education’s assistant superintendent for business services, told the Lost Coast Outpost this morning that McKinleyville Union’s $4.2 CAB issuance represented the second round of bonds authorized by Measure C. The first, which amounted to some $7 million, was structured in a far more conventional manner. But when, in 2011, it came time for the district to raise more cash, it was already bumping up against the school bond tax rate cap imposed by the state of California, which allows a district to levy no more than $30 per year for every $100,000 worth of property value. The CAB structure on the additional $4.2 million allowed the district to push repayment way into the future in order to avoid these limits.

(The county’s Office of Education, it should be said, has no input on how local school districts choose to structure their debt. Once the electorate approves a bond issue, as both the Fortuna High School and Arcata Elementary School did in the most recent election, the decision on how to structure those bonds is up to the school board in question.)

Humboldt County Superintendent of Schools Garry Eagles told the Lost Coast Outpost that capital appreciation bonds are a last-ditch measure, the responsibility for which ultimately lies with state government. After Proposition 13, which limited the ability to hike property tax, it’s extremely difficult for local districts to pass pay-as-you-go measures that would avoid heavy interest charges, and state government — hampered by the same initiative — hasn’t stepped up to fill the bill.

“There are not many finance options for local school districts,” Eagles said.

In the LA Times story, Lockyer likens capital appreciation bonds to the shady deals and trickery employed by Wall Street in the run-up to the mortgage crash. Hanger said that he has seen proposed regulation that he expects will tackle the issue in the next state legislative session — by capping the terms of the bonds, the the total allowable debt ratio or through some other measure. In the meanwhile, though, it’s interesting to note that the school board that runs McKinleyville Union — the most shocking local example of out-of-scale borrowing — counts among its trustees several high profile members of the local business community: Brian Mitchell of Security National, Tim Hooven of Hooven & Co. and Justin Zabel, CEO of Mercer-Fraser.

School districts are able to justify the high debt ratios involved in many capital improvement bonds by speculating on dramatically increased property tax revenue. As the General Plan Update moves forward, and as the McKinleyville community continues to protest proposed new rates of development, it should know that its school board has already taken those numbers to the bank.

CLICK TO MANAGE