A medical examination room in Fresno on June 8, 2022. Photo by Larry Valenzuela, CalMatters/CatchLight Local

Brian Iv works in a factory in Orange County, earning around $26 per hour. He suffers chronic pain from a lifetime of manual labor jobs and previous workplace injuries, but often treats the pain with home remedies or traditional Cambodian practices. Going to the doctor is too expensive, he said.

Iv recently got a raise and was able to purchase health insurance through his company, but for a long time he had a Covered California Silver Plan, a mid-tier plan under the state’s version of the federal Affordable Care Act marketplace. A visit to a primary care doctor cost nearly $50, and every time Iv picked up a prescription it was an additional $10 to $15. It was a lot for someone living paycheck-to-paycheck with little wiggle room in the budget.

“Right now, after COVID-19, everything is expensive,” Iv said. “Sometimes when you get sick you avoid that (expense). You have to keep the money to pay the rent, pay the bills, pay the car.”

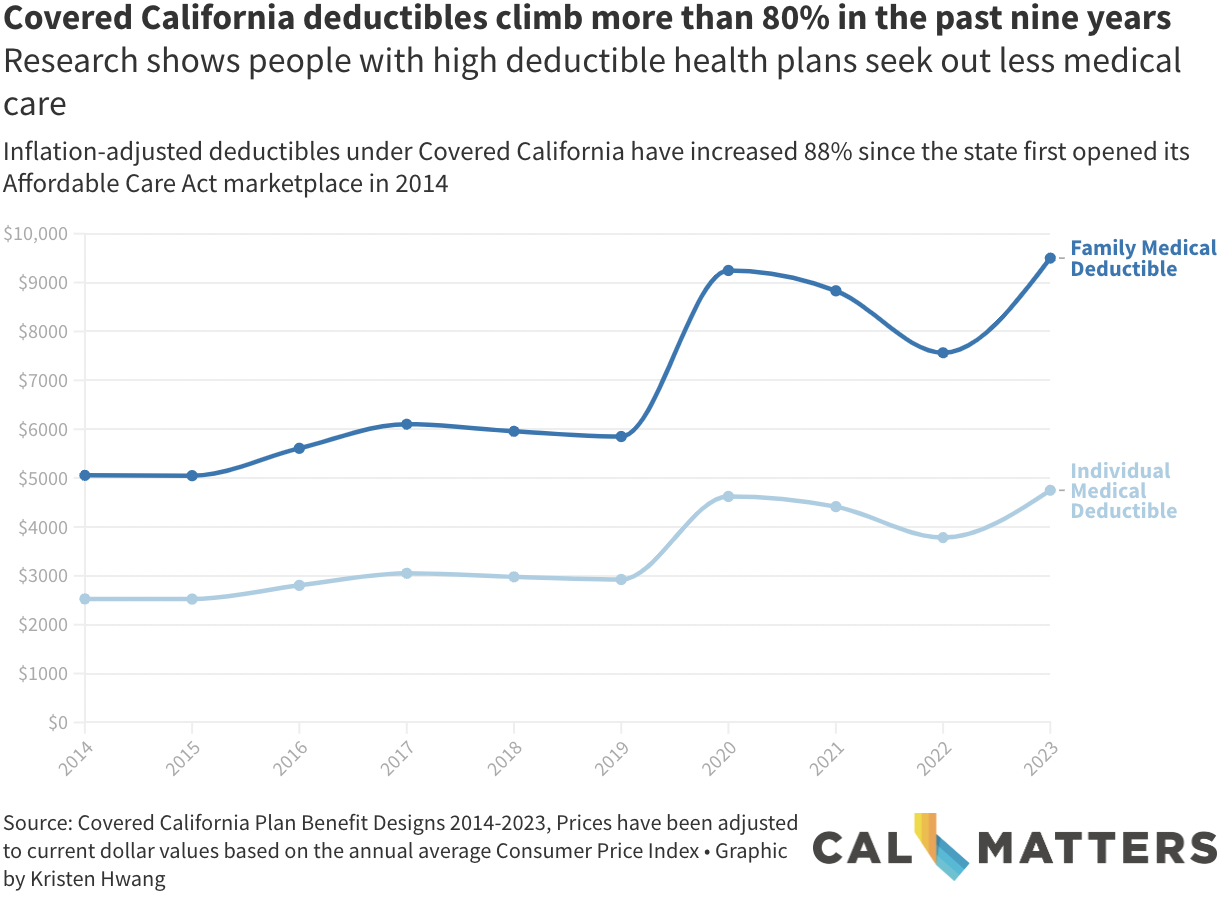

Mid-tier health coverage like Iv’s Silver Plan is widely considered the best value for people who have insurance through Covered California. But in the past nine years, deductibles for the Silver Plan have grown nearly 88% after adjusting for inflation, increasing out-of-pocket costs for enrollees. In raw numbers, last year deductibles grew from $3,700 for an individual and $7,400 for a family with a Silver Plan to $4,750 and $9,500, respectively.

That’s why health care advocates are miffed that Gov. Gavin Newsom’s budget proposal would sweep away $333.4 million set aside a couple of years ago for the state to defray health care costs for middle-income residents, transferring the money to the general fund. The proposal to move money out of the Health Care Affordability Reserve Fund is temporary, with plans to restore it in 2025 when current federal subsidies expire. But advocates say inflationary pressures and rising health care costs are reasons to use that money right now to help Californians struggling to pay the bills.

“We recognize there’s not a lot of room for new spending in the current budget situation, but we don’t see this as new spending. We see this as the existing commitment,” said Diana Douglas, policy director for Health Access California, which sponsored legislation to create the reserve fund.

The budget transfer idea is part of Newsom’s strategy to address a projected $22.5 billion deficit this year, a deficit that the nonpartisan Legislative Analyst’s Office predicts may be even worse come May when the budget will be revised based on actual state revenue.

Newsom’s spokespeople ignored multiple requests for comment.

Given the inflationary pressure people like Iv face, the governor’s proposal to transfer the money into the general fund is “mystifying,” said Scott Graves, director of research at the California Budget and Policy Center, a nonprofit policy research group.

“Why is the governor borrowing from a special fund that was set up specifically to help make health coverage through Covered California more affordable, right?” Graves said. “This is money for which every penny in the account could right now be used to bring down the cost of health care for Californians, but instead the governor is choosing to sweep that money out of the account.”

Stories like Iv’s are common, said Jaquelinne Molina, a caseworker at The Cambodian Family, a social services center where Iv receives case management for health care and financial aid issues. Most of the people she serves work in warehouses and factories for low pay and no benefits.

“It’s three years after COVID, but people are still behind on their light bills, their water bills from 2020 because they weren’t able to work due to COVID,” Molina said. “Right now everything is tight and it gets harder and harder every year.”

Broken promise?

Health care advocates say Newsom’s latest budget proposal follows a pattern of missed opportunities to make insurance more affordable under Covered California.

In 2020, the Legislature voted to reinstate a tax penalty on residents without health insurance in an effort to bring costs down. The economic theory goes: The penalty incentivizes people to buy health insurance, and the more people who participate in the health care marketplace, the lower the costs because risk is spread out among a mix of healthy and less-healthy consumers.

But that measure passed despite concern from advocates and legislators about forcing people who can’t afford insurance to purchase it. Most people who forego insurance cite high cost as the primary barrier.

“Advocates, including ourselves, clearly stated that we do not support the reinstatement of the penalty without additional assistance,” said Linda Nguy, a lobbyist for the Western Center for Law and Poverty.

Early on, that was the plan. In fact, on his first day in office, Newsom proposed using the money to bring down prices for people with Covered California.

“The governor, to his credit, proposed this idea of providing state subsidies in Covered California, augmenting the federal dollars, and proposed the individual mandate as a funding source for it,” Health Access Executive Director Anthony Wright said.

Influential advocacy groups supported reinstating the health insurance penalty, and the 2019-2020 budget included more than $1.4 billion over three years to bring down out-of-pocket costs for Covered California enrollees.

So far, the state has only kept that promise once, spending approximately $355 million in 2020 to enhance Covered California subsidies for middle-income residents. This meant an individual making up to $74,940 and a family of four earning up to $154,500 qualified for additional financial assistance. But when the federal government increased health care subsidies in 2021 as part of its COVID-19 pandemic relief package, the state stopped funneling penalty money toward cost reduction.

Kaiser Health News reported in November that the state has generated roughly $1.3 billion in penalty money from uninsured state residents. By statute, that money has always gone directly into the general fund, and from there could be moved into the reserve fund.

“There’s an argument to be made that those fines really should be plowed back into the system, especially for people who are low-income,” said former state Sen. Richard Pan, a doctor who chaired the health committee at the time the penalty was reinstated.

The remaining $1 billion originally budgeted for subsidies in 2021 and 2022 — roughly the same amount generated by the penalty — has never been spent on bringing down health care costs. Instead, it has stayed in the general fund.

“What we think has been happening, and there truly is not a lot of transparency on this, is that as money is put into the reserve, it is taken out the following year,” Douglas with Health Access said.

Who relies on Covered California?

Most people who purchase insurance through Covered California are low- to middle-income Californians, meaning individuals who earn roughly between $21,000 and $87,000 a year or families of four earning $45,000 to $180,000 per year.

At that income level, enrollees make too much money to qualify for Medi-Cal, the state’s public insurance for very low-income residents, but for a variety of reasons don’t have employer-based health insurance. They may be self-employed, a gig or part-time worker, or work for a small business. They may even opt to purchase insurance independently because it’s cheaper than what their employer offers.

Although more stable than the national insurance marketplace, Covered California has not been immune to the rising health care costs that plague the industry. Health insurance premiums have grown every year since the state first offered Covered California. That growth is less obvious than deductibles to enrollees because federal subsidies keep out-of-pocket premiums relatively stable for most enrollees. But federal subsidies are based on federal income limits and poverty levels, which don’t take into account California’s high cost of living.

Brian Iv in Santa Ana. Photo courtesy of The Cambodian Family

Brian Iv in Santa Ana. Photo courtesy of The Cambodian Family

Iv and his family rent a single room in a house in Garden Grove for $900 a month. In the past year, he said, expenses have tripled with inflation, with gas alone costing around $300 per month.

“At home, sometimes we don’t know what to cook and we don’t have food. Then we eat Cup Noodles,” Iv said.

Molina, the case worker from The Cambodian Family, said her clients who have deductibles and co-pays use their insurance less than clients with Medi-Cal, who typically don’t have to pay anything out-of-pocket.

“I’ve known families with kids who break or sprain their fingers and feet, and they don’t know for months because they can’t go to the doctor,” Molina said.

The federal government’s relief plan helped people afford Covered California. It lowered monthly premiums by 20%, and more than 90% of enrollees were eligible for financial help. The result was a record number of people signing up for health insurance last year: 1.8 million, a 9% bump from the previous year.

But when the American Rescue Plan was at risk of expiring in 2022, legislators and regulators saw an opportunity to lessen the staggering health insurance costs enrollees would face — double what they paid the year before. They proposed reinjecting penalty money back into the Covered California marketplace, as promised, for the first time since 2020.

In June, the Covered California board approved a $300-million cost-reduction plan: If the federal subsidies were not renewed, the money would be used to help alleviate the resulting out-of-pocket premium spikes. If subsidies were extended, the money would be used to eliminate deductibles for all Silver Plans.

Either way, the money would make health care more affordable. When the federal government opted to extend premium assistance until 2025, affordability advocates were excited by the chance to remove other cost barriers.

“Let’s get rid of deductibles,” Pan said. “Because what is a deductible? It’s just really a barrier to people being able to get care.”

To enforce the plan, Pan carried and Health Access sponsored a bill that would have required the state to bring down costs for Covered California enrollees. Newsom vetoed the bill, citing a “downturn in revenues” despite the state budget already including more than $300 million to implement the plan.

When the bill died, Covered California lost the ability to implement the plan, said James Scullary, spokesperson for the program. Instead, Silver Plan deductibles that would have been eliminated jumped about 20%.

“Covered California’s position is we are always looking for ways to make health care more affordable,” Scullary said. While deductibles have climbed, pharmacy costs decreased and out-of-pocket maximums remained relatively stable.

Some advocacy groups say they’re dismayed that increased cost-sharing is “not a priority for Gov. Newsom.” The majority of small business owners are middle-income Californians who often have trouble affording health insurance and find it too expensive to offer to their employees, said Bianca Blomquist, California policy and outreach director for the Small Business Majority.

“We are super disappointed,” Blomquist said. “If we’re talking about small businesses’ ability to recover from the pandemic, these are the kinds of programs that might not be obvious, but really help.”

###

CalMatters.org is a nonprofit, nonpartisan media venture explaining California policies and politics.

CLICK TO MANAGE